The Unseen Premium: Why Raising National Insurance is the Collective Car Insurance We Can No Longer Afford to Skip

- Peter Middleton

- 6 hours ago

- 6 min read

If you glance at your payslip at the end of the month, your eyes probably dart straight to the biggest numbers: your gross pay, the income tax deduction, and that final, crucial net figure that lands in your bank account.

But there’s another line item sitting quietly next to income tax, one that has been the focus of fierce political debate, policy shifts, and front-page news lately: National Insurance Contributions (NICs).

To many, National Insurance feels like a duplicate tax. It’s deducted from our earnings, or levied on employers, and flows into the vast registry of state finances.

When governments change National Insurance, whether by lowering employee rates or raising employer contributions, the public often responds with frustration and fatigue. Why do we pay it? What does it actually fund? And in today’s economic climate, why does increasing it make sound, practical sense?

To understand the value of National Insurance, we have to look past the dense spreadsheet terminology of HM Revenue and Customs. We need to look at it for what it truly is: a collective, nationwide insurance policy.

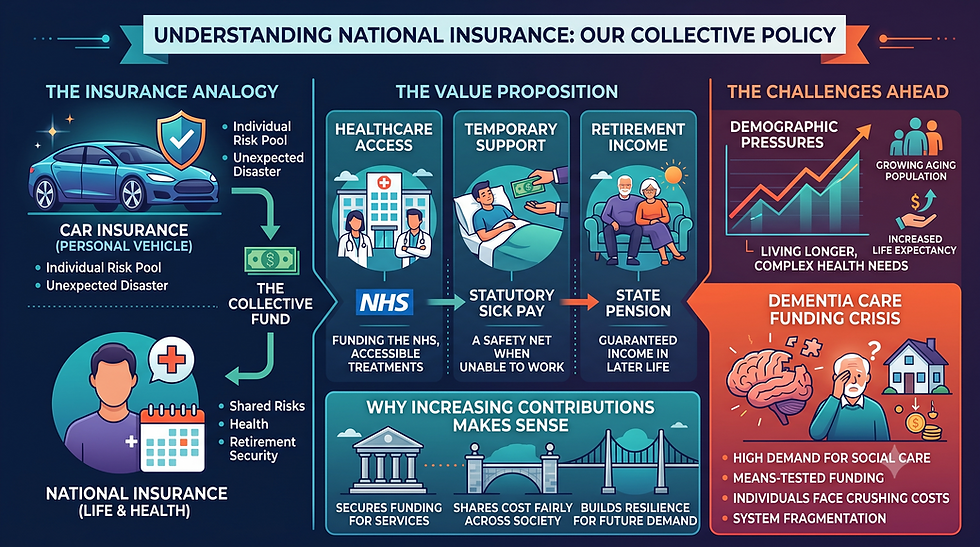

The Great British Car Insurance Analogy

Think about the car sitting on your driveway. By law, you can’t drive that vehicle on a public road without third-party insurance. Most of us opt for comprehensive cover. Every year, you pay a premium to an insurance provider.

When you pay that premium, you don’t expect a payout the following week. In fact, you actively hope you never have to make a claim.

You don’t hand over £500 to an insurer and think, "I can’t wait to write my car off in November to get my money’s worth."

Instead, you pay for peace of mind and shared risk.

You pool your money with millions of other motorists.

If you have a flawless year of driving, your premium helps cover the cost for the driver who hits a patch of black ice or suffers a cracked windscreen.

It’s an unwritten social contract of the road: we all pay a manageable amount so that an unexpected disaster doesn’t completely bankrupt any single one of us.

National Insurance functions on exactly the same principle, but the stakes are infinitely higher. Your body, your health, and your old age are the vehicle.

THE INSURANCE ANALOGY | |

CAR INSURANCE | NATIONAL INSURANCE |

Protects your vehicle | Protects your life & health |

Pools risk with other drivers | Pools risk with the nation |

Paid to avoid catastrophic repair bills | Paid to avoid social crash |

THE FUNDAMENTAL TRUTH | |

If the cost of repair rises, the premium must adjust. | |

When you pay NI, you are not simply funding general government projects or filling a generic treasury black hole. You are paying a premium into a system designed to protect you from the catastrophic hazards of life:

The breakdown service: The National Health Service, treating you when your physical gears grind to a halt.

The courtesy car: Statutory Sick Pay or Employment and Support Allowance when you are temporarily out of action.

The retirement plan: The State Pension, ensuring that when your working life reaches its natural destination, you have a baseline of financial security.

Now, consider what happens to your car insurance premium if the cost of car parts skyrockets, if vehicle thefts double, or if the roads become significantly more treacherous.

The insurance company recalculates the risk and raises the premium. If they kept premiums exactly the same while repair bills tripled, the firm would go bust, claims would go unpaid, and stranded drivers would be left on the hard shoulder.

This is precisely where the UK finds itself. The cost of repairing and maintaining our collective social vehicle has risen dramatically. Pretending we can keep paying the same old premiums while expecting first-class repairs is a mechanical impossibility.

Why Raising the Premium Makes Sense

No one likes paying more. Whether you are an individual watching your net pay shift or a business owner managing payroll costs after recent adjustments, an increase feels like an extra burden. For instance, recent budget changes raised the employer National Insurance rate to 15% and lowered the threshold at which they start paying it to £5,000.

While these shifts cause structural adjustments for businesses across the country, we have to look at the macro perspective. Why does raising National Insurance make structural sense over other forms of taxation?

1. It’s directly linked to the social contract.

Unlike general VAT or fuel duty, National Insurance is visible, trackable, and conceptually tied to our social safety net. It reinforces the idea that if you work and participate in society, you are actively earning your stake in its protection.

When the public knows that revenue is earmarked for the health and welfare of the community, there’s a clearer line of sight between the sacrifice (the deduction) and the benefit (a functioning healthcare and pension system).

2. We are living longer, more complex lives.

When the modern welfare state was constructed in the mid-twentieth century, life expectancy was significantly lower. People retired, drew a pension for a few years, and required relatively basic medical intervention before passing away.

Today, we are experiencing an incredibly positive human achievement; we are living much longer.

However, living longer means our medical needs are vastly more complex. We are surviving conditions that used to be fatal, requiring decades of ongoing management, prescription medication, and specialised care.If our collective vehicle is running for twice as many miles, the maintenance costs will inevitably increase.

3. Protecting the foundational infrastructure.

If you refuse to pay to patch a small leak in your house, you eventually end up paying ten times as much when the roof collapses. Raising NI is an act of structural preservation.

By stabilising the funding base for the NHS and state benefits, we prevent a total systemic collapse that would cost individual citizens far more in private alternatives, lost productivity, and social instability.

The Darkest Corner of the Garage: The Dementia Care Crisis

If National Insurance is our comprehensive breakdown cover, there’s one major, devastating mechanical failure that the policy currently fails to cover adequately: dementia care.

Dementia is the defining health and social care challenge of our time. There are nearly one million people living with dementia in the UK right now, and that number is projected to climb to 1.4 million by 2040. Yet, despite its prevalence, the way we fund dementia care is deeply fractured and profoundly unfair.

To return to our car analogy, imagine discovering that your comprehensive insurance policy covers engine faults, brake failures, and electrical glitches, but if your gearbox breaks, the insurer steps back, folds their arms, and says, "Sorry, that’s a cosmetic issue. You’re on your own."

The Dementia Divide: If you suffer a heart attack or cancer, the NHS covers your treatment entirely, from diagnosis to surgery and hospital stays. But if you develop Alzheimer’s disease or vascular dementia, the system largely classifies your long-term needs not as “healthcare” but as “social care”.

Because social care is means-tested in the UK, the state only steps in if your personal assets fall below a very low threshold. The current financial reality of this policy is staggering:

METRIC | THE REALITY OF DEMENTIA CARE |

Annual Cost to the UK Economy | £42 billion, rising to £90 billion by 2040. |

The Family Burden | 63% of all dementia care costs are paid for by patients and their families. |

Weekly Cost | Average residential dementia care runs at approximately £1,375 per week. |

Unpaid Care | A third of unpaid family carers spend over 100 hours a week providing support. |

Nearly half of all people entering residential or nursing care have to fully fund it themselves. They are forced to sell their family homes, liquidate their life savings, and watch their hard-earned inheritances vanish simply because they suffered a disease of the brain rather than a disease of the heart.

This is the lack of funding for dementia care in plain sight. It’s a lottery of illness.

Why a Higher Premium Benefits the Whole System

This glaring gap in dementia care is precisely why a robust, properly funded National Insurance framework is so essential. Social care and healthcare are not two separate systems; they are two sides of the same coin.

When social care is underfunded, the NHS clogs up. Patients who are medically fit to leave hospital wards can’t be discharged because there’s no dementia care placement or home-support package available for them. This causes a backlog that ripples through to A&E waiting rooms and ambulance response times.

By recognising that our collective insurance premium needs to rise, we create the financial headroom required to address this crisis. We can begin moving toward a society where dementia care is treated with the same systemic dignity as any other terminal condition, sharing the financial risk across the entire population rather than letting it crush individual families.

Conclusion: Securing the Road Ahead

No one celebrates an increase in insurance premiums. It’s completely understandable to view rising contributions with a heavy heart, especially when household and business budgets are already stretched.

But we have to ask ourselves an honest question: what is the alternative?

If we refuse to adjust our contributions, we are choosing to drive a deteriorating vehicle on crumbling roads, hoping against hope that we don’t break down.

National Insurance is the mechanism that keeps our society moving. It ensures that when you get sick, grow old, or your mind begins to fail you, you are not cast aside to cope alone. Raising these contributions is not an act of bureaucratic greed; it’s a necessary, clear-eyed investment in the collective peace of mind that defines a decent, compassionate society. It’s the price we pay to ensure that no matter how rough the road gets, none of us are left stranded by the side of it.

It’s time to insure to ensure all of our futures.

Comments